<< Lesson 3

Lesson 5 >>

Lesson Overview – this lesson outlines some important fundamentals of economic systems as well as the effects of government intervention on the market

The classical economics theory can be whimsical and Utopian, especially in developing countries. Nevertheless, classical economics will remain the foundation stone that holds everything in place. Every other contemporary sub-discipline of economics has a place and origin in classical economics. Much of the problems and challenges forming mainstream development economics stem from certain failings of classical economics. Therefore, it is imperative to cover some of those fundamental issues as this section does. Let us begin with the basic economic problem.

3.1 THE BASIC ECONOMIC PROBLEM

The basic economic problem is scarcity. It is the challenge that comes with meeting unlimited[1] needs with limited resources. It may be because of the Basic Economic Problem why our world is constantly caught in the trap of bickering and conflict. The basic economic problem is by and large why we have plenty of terrible headlines each time we switch on the TV as shown in Figure 4.

Figure 4 Role of Basic Economic Problem in conflict

Due to the basic economic problem, three questions arise. These are What, How and for whom. Any given society/country must decide how it will answer these questions. In other words, any given society must choose an economic system/market system, or rather the right mix of these. There are three types of economic systems. These are free market economy, centrally planned (command) economy and the mixed economy system. The next section discusses these economic systems in slightly greater detail.

3.2 MARKET SYSTEMS

3.3 CENTRALLY PLANNED (COMMAND) ECONOMY

The centrally planned economy is characterised by no private ownership of resources or factors of production. Prices are determined and set by the government, while decisions in the economy are centrally made or planned by the government because it owns and controls all the resources. In a centrally planned economy there is no freedom of choice because the government determines what, how and for whom output would be produced for. There is no competition, and there is no freedom of choice on the part of consumers and owners in terms of desire for ownership. The command economy’s main objective is to protect the welfare of society.

This economic system has a number of advantages and disadvantages. The first advantage is that the gap between rich and poor is closed under the command economy. The centrally planned economy results in equitable income or wealth distribution. Additionally, consumers are better off because the main objective is the welfare of society. Prices are also affordable since they are set by the government. However the system is not without some disadvantages. Under the command economy, the quality of life is reduced because consumers are not free to choose the commodities and services they want. The system also does not promote satisfaction of customer needs and wants. Another disadvantage is that resources are allocated inefficiently because prices are set below equilibrium price which compromises availability and quality of production. The distributive mechanism may suffer from corrupt tendencies and nepotism by the responsible people although the intentions are good.

3.4 FREE MARKET ECONOMY

It is founded on the ideals of capitalism. This has been the dominant feature of the developed world. In terms of characteristics, profit maximization features as a major objective. In such as system there is no government intervention on the market and there is freedom of choice. It means that consumers are able to buy goods and services they want while producers have the same liberty when it comes to production and provision services. There is private ownership of resources and prices are determined by the market forces of demand and supply. There is competition in the market.

This type of system enjoys a number of advantages. It results in efficiency because the profit objective compels producers to produce at the lowest possible cost. Freedom of choice ensures there is societal welfare by upholding preferences and tastes. Prices are determined by the market forces of demand and a supply therefore they are set at the equilibrium or optimum. Prices are an important aspect in the economy because they act as market signals. If prices are too high in a certain section of the market this could be an indicator that adequate resources are not being channeled to that section to meet overwhelming demand. In addition, the existence of competition compels firms to invest in the research and development of new and quality products so as to be competitive.

Nevertheless, this system is also fraught with challenges. Since profit is the main objective, the actions of firms in pursuit of profit may be detrimental to society. There is also a danger of the markets turning into monopoly markets that may be characterized by overpricing through price discrimination. The system benefits the rich more than the poor as they continue to get rich since they are employers while the poor, as the workers continue being poor. In this system resources remain in the hands of the rich, especially in terms of natural endowments such as mines./

3.5 MIXED ECONOMY

Between the two extreme versions of economic systems mentioned earlier, there is the mixed economy. In a mixed economy the policymaker simply takes the best of everything and hopes for the best. In a mixed economy system some resources are owned by the government while some are owned by the private sector. Government sets prices on selected commodities while the rest are determined on the market. Competition is allowed to exist although there may be competition laws that prohibit certain practices. In terms of advantages it takes merits after both the command and free market economies. The same can also be said about the disadvantages of this system.

3.6 THE VERDICT – WHICH IS THE BEST MARKET SYSTEM?

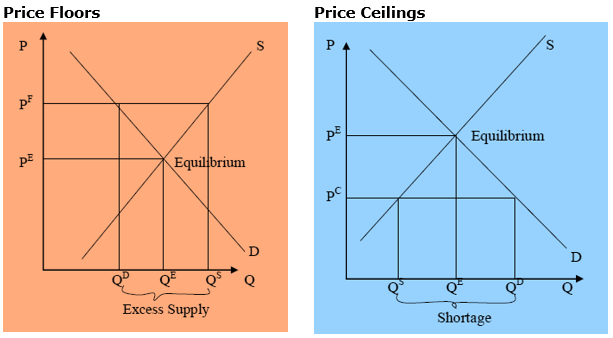

The Centrally Planned Economy is very problematic mainly because of the disadvantages already discussed. Perhaps the biggest problem of the centrally planned system lies in the fact that prices are set below equilibrium price in order to make them affordable, thereby creating shortages. To protect and support producers, the government may set prices above equilibrium prices – thereby short-changing consumers since they would be paying more than they have to. This type of government intervention on the market is commonly known as price controls. The two forms of price controls are price ceiling and price floor as shown in Figure 5.

Figure 5: Consequences of Price Floors and Price Ceilings

D represents the Demand Curve or Demand Function. The Demand Curve is the inverse relationship between Price (P) and Quantity Demanded (Qd). It stems from the Law of Demand which states that consumers will buy more at a lower price than at a higher price. S represents Supply Curve or Supply Function. The Supply Curve is the geometrical relationship between Price (P) and Quantity Supplied (Qs). It stems from the Law of Supply which states that suppliers will produce more at a higher price than at a lower price. The equilibrium prices and quantities are arrived at when D meets S, and without government intervention these would be PE and QE. At the price ceiling consumers demand a quantity QD while producers would supply QS. There is a shortage QD – QS. The price floor will result in consumers demanding a quantity QD while suppliers would supply QS. Therefore there is a market excess QS – QD .

3.7.1 PRICE FLOORS

- Inefficient producers are protected at the expense of society.

- Tax payers are worse due to the increased government expenditure which results from buying the excess off the market by the government in order to maintain the price floor.

- Consumers pay artificially high prices.

3.7.2 PRICE CEILINGS

- There is a massive shortage of the commodity on the market.

- There is emergence of the parallel market and consumers are charged prices even higher than the original equilibrium price (PE) that would have existed without intervention.

- If the government does not intervene further the shortage will bid up the price back to PE.

3.8 FURTHER MERITS OF THE FREE MARKET SYSTEM

Adam Smith is regarded as the Father of Economics. In his book “Wealth of Nations”, he popularized the idea that the government should respect free markets and let economic agents carry out market transactions without the intervention of the government since this led to more efficient outcomes. This is because due to self-interest, economic agents will embark on actions that maximize their benefit or example, a farmer selling his/her produce at a price that gives him/her the best profit but also minding the fact that consumers’ are self-interested in value for money. Hence the market price arrived at through all these interactions is the right price i.e, Price (P) = Marginal Cost (MC)[2]. The market efficiently works in this instance because of the invisible hand – where it is possible to predict human behaviour – also known and economic rationality (utility maximization).

Without government intervention, competition can either be perfect or imperfect. The preferred one is perfect competition. Under perfect competition, prices are marked at the least price (economic price) or at the point where P=MC. Some of the Main assumptions of Perfect competition are:

- Many (unlimited) buyers and sellers

- No barriers to entry

- Perfect information (no information asymmetry)

- No collusion

This is discussed in more detail in the next section.

Activity 3

- Can we think of unsavoury industries that exploit any of these assumptions?

- Can we think of industries where there are barriers to entry?

- What are some of those barriers to entry?

- How can scientists address some of the barriers or market imperfections?

[1] An important axiom of the theory of consumer behaviour is that “more is preferred to Less”. This is an inherent human characteristic as each of us seek to maximise our utility/satisfaction

[2] Marginal cost is the cost of producing an additional unit of output. Thus a unit of out has an interest component (to pay for capital cost), a wages element (to pay for labour), a rent element (to pay the cost of land) and a normal profit element (to pay the reward for starting a business). Hence the factors of production we have here are capital, labour, land and someone to organize and direct everything. Note, the use of the term normal profit. This is a fair – market determined profit. Where there is imperfect competition, businesses make abnormal (large) profits at the expense of consumers.